Credit Report Explained: How to Read it Properly

In our society today, the credit report is a critical document that records your financial profile from a debt borrowing and repayment standpoint. By aggregating all your outstanding debts together in one place, the report enables the user to see how well the borrower has managed to repay debts on time across multiple accounts. These accounts include everything from credit card bills, personal loans, and auto loans to student debt, revolving lines, utility payments, and even telecommunications bills. Mortgages may also be included depending on the credit agency used. All of this information is then put together into a single three-digit score called your credit score which ranges from 300 to 900 (with 900 being the best score you can get).

Where is it used?

Because of this ‘snapshot’ nature of the credit report, it is a major tool used by lenders when evaluating whether the borrower is creditworthy or not. Assuming that the borrower is deemed to be creditworthy, the credit score can also inform key terms of the loan including pricing and amortization. In general, a better credit score generally opens up access to more favourable terms and conditions as the credit risk of the borrower is perceived to be lower the higher up the credit score ladder they are.

Despite its importance in applying for new credit, the credit report may not always be intuitive to read. Notwithstanding that, understanding your credit report is a key skill. As such, this article delves a little bit into the nuances and details that need to be kept in mind when evaluating your credit report prior to applying for a new loan.

Credit Report Basics

At a fundamental level, every credit report will have your personal information including full name, date of birth, current and most recent previous addresses, social insurance number, passport number/driver’s licence (if applicable), and current and previous employers you have worked with. This is essentially used as an identifier to validate that the correct credit report has been pulled, and provides the user (such as a lender) to see the borrower’s previous employment and residential addresses.

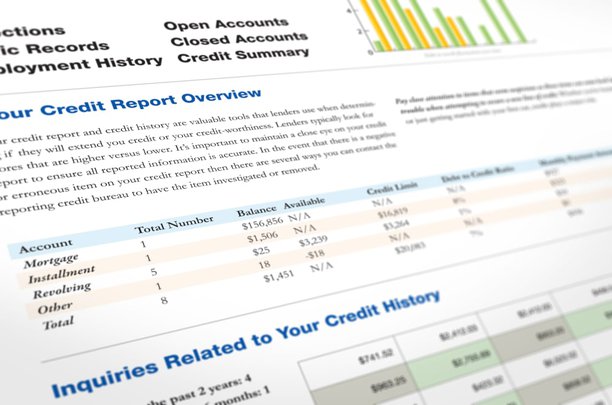

Credit History

Once lenders have validated the basic information of borrowers listed above, the next and most important step is to assess their credit history. This will include all currently open credit accounts including lines of credit, credit cards, utility/mobile bills, and secured and unsecured personal loans that the borrower has taken out. Retail and store cards are also included in a credit report. Other information includes:

Non-sufficient fund payments or cheques that were ‘bounced’;

Credit accounts that were closed due to fraud conducted by the borrower;

Bankruptcy or court decisions that relate to credit;

Lender inquiries made on the borrower’s file;

Debts that have been transferred to collections agencies;

Liens on existing property and assets that have been pledged to lenders.

With regards to specific credit accounts, the credit report will also contain information such as when the account was opened, how much is currently owing on the account, if payments have been made on time, and/or if the credit limit was breached at any time. Additionally, negative information such as missed payments, transfers to collections agencies, and/or bankruptcies that have been recorded will also be seen for a certain period of time. While each Province sets its own rules for how long negative information can be seen on the credit report, it generally ranges between 6 to 7 years.

How do you read a credit report?

When lenders and other creditors send a borrower’s information to credit reporting agencies, each account will come with 2 items: (i) a letter that represents the type of account being reported, and (ii) a number that represents the repayment profile of the borrower on the account. Let’s start with the letters first:

I (Installment): The letter ‘I’ is used to denote loans with fixed repayments that have to be made at the end of each period until the loan is paid back. Some examples of this loans that will be classified ‘I’ include student loans, personal loans, and car loans.

O (Open): The letter ‘O’ is for loan facilities where the borrower may borrow money when he/she needs to, but only up to a certain limit. A phone/hydro bill and/or line of credit is an example of a loan that would be classified ‘O’.

R (Revolving): For revolving credits where progressive amounts can be borrowed (and are repaid depending on the amount outstanding), the letter ‘R’ is used. A credit card is a good example of a type of facility that would be classified as ‘R’.

M (Mortgage): Not every credit agency reports on mortgages. However, if they do, then the letter ‘M’ will be used to denote mortgages held by the borrower.

Next, let’s take a look at what the numbers indicate on a credit report. Each account is assigned a number between 0 to 9. The list below shows what type of repayment pattern each number corresponds to:

0: This generally means that the account has been newly created. For example, if a credit card has been recently approved, but not yet used, it will have ‘0’ besides it.

1: The number 1 would indicate that the credit account is being paid as agreed. This is the most favourable place to be from a borrower standpoint.

2: Payments that are 31 – 59 days late have the number 2 assigned to them.

3: Payments that are 60 – 89 days late have the number 3 assigned to them.

4: Payments that are 90 – 119 days late have the number 4 assigned to them.

5: Payments that are 120+ days late, but not yet written off by the creditor or lender.

6: Code is not used in a credit report

7: Payments that have gone into a debt management program or consumer proposal where a set repayment schedule has now been agreed upon.

8: Repossession of borrower assets

9: Debts that are written off as bad debts, sent to collection agencies, or where the borrower has declared bankruptcy are classified as 9.

Now that you are more familiar with deciphering what the information on your credit report really means, you should hopefully be better positioned to manage your credit score more prudently, and take the corrective steps (if needed) to improve the way your credit report looks.